-Mr Mortgage

Jim Pendleton

ALL 50 States -

Affiliated Federal Bank

Call 631-451-7400 or

click/Text 631 512-1248

2021 Financial Services of America, LLC

Jim Pendleton NMLS 684537 ALL RIGHTS RESERVED

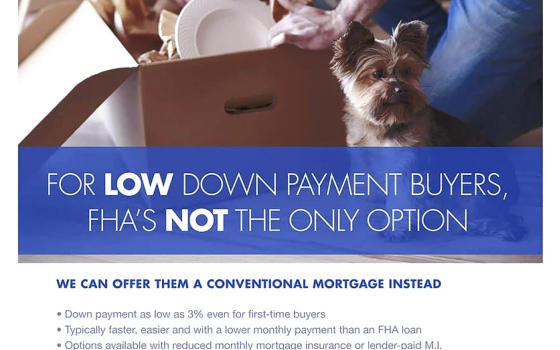

CONVENTIONAL MORTGAGE

A Program offered by most Financial Institutions

What is a 30-Year Fixed Mortgage?

A 30-year fixed mortgage is a mortgage that has a specific, fixed rate of interest that

does not change for 30 years. 30-year fixed mortgages are the most popular

mortgage product nowadays and are especially popular among first-time home

buyers.

If you choose a 30-year fixed mortgage, your monthly payment will be the same

every month for 30 years. However, the breakdown of how much of your mortgage

payment goes to principal and how much goes to interest will shift throughout the

lifetime of the loan. Your payments will be spread over 30 years, with the interest

payments making up the majority of the payment at the beginning, and then principal

paid off toward the end of the term.

Advantages of a 30-Year Fixed Mortgage

Easier to budget the rest of your monthly expenses because your mortgage

payment is the same amount every month.

Lower monthly payment in comparison to other mortgage products.

The 30-year time period is more appropriate if you plan on living in your house for

a really long time or indefinitely.

Because your mortgage payment is generally lower, it frees up cash for

emergencies, to pay off other debt that has higher interest, or you can use it to

diversify your investments.

When rates are low, you may want to lock in a really great low fixed rate.

What is a 30-Year Fixed Mortgage?

A 30-year fixed mortgage is a mortgage that has a specific, fixed rate of interest that

does not change for 30 years. 30-year fixed mortgages are the most popular

mortgage product nowadays and are especially popular among first-time home

buyers.

If you choose a 30-year fixed mortgage, your monthly payment will be the same

every month for 30 years. However, the breakdown of how much of your mortgage

payment goes to principal and how much goes to interest will shift throughout the

lifetime of the loan. Your payments will be spread over 30 years, with the interest

payments making up the majority of the payment at the beginning, and then principal

paid off toward the end of the term.

Advantages of a 30-Year Fixed Mortgage

Easier to budget the rest of your monthly expenses because your mortgage

payment is the same amount every month.

Lower monthly payment in comparison to other mortgage products.

The 30-year time period is more appropriate if you plan on living in your house for

a really long time or indefinitely.

Because your mortgage payment is generally lower, it frees up cash for

emergencies, to pay off other debt that has higher interest, or you can use it to

diversify your investments.

When rates are low, you may want to lock in a really great low fixed rate.

With over 45% of buyers purchasing a home for the first time, a big chunk of home

buyers are newly experiencing the fierce complexities and challenges of buying a

home. And financing is, without a doubt, an important factor for those looking to own.

Most buyers (77%) obtain a mortgage to finance their home, according to the Zillow

Group Consumer Housing Trends Report 2018. Before you take on the responsibility

of a mortgage, take a look at what many first-time home buyers wish they knew

about financing.

Down Payments & the Myth of 20%

Even though most buyers have get a mortgage to finance their home, they usually

will also need a lump sum of cash to put towards a down payment — a hurdle that

prevents many would-be buyers from making the leap to homeownership.

But just because you don’t have a huge down payment doesn’t mean you can’t buy.

Despite common misconceptions about home financing, a 20% down payment is not

a requirement for homeownership. Although buyers who don’t put down a full 20%

typically have to pay a premium for the extra risk lenders take — private mortgage

insurance (PMI) — they may still be in a situation that’s more financially

advantageous than paying monthly rent payments.

Zillow’s report found less than a quarter (23%) of buyers put 20% down, while 52%

put less than 20% down. So while down payments have once been seen as the

biggest hurdle to homeownership, many first-time home buyers are finding ways

around the 20% myth and landing their homes anyways.

Loans Aren’t One-Size-Fits-All

Just as homes come in various styles and at different price points, so do the ways

you can finance them. There are a number of loan options to choose from, but

deciding which kind is best for you requires a little bit of time and research.

Many home shoppers assume the best choice is the ever-popular 30-year fixed loan,

which offers the advantage of a set interest rate, regardless of how the market rises

or falls. But if you don’t plan on living in your home for 20 or 30 years, an adjustable

rate mortgage (ARM) could be a choice to consider. This loan type allows you to get

a lower initial interest rate compared to a fixed-rate mortgage, but it isn’t guaranteed

to remain at that rate, so be sure you understand how much the interest rate could

change before selecting that loan type.

If a low down payment or low credit score is your primary hurdle, a government-

backed loan might be a good option. Federal Housing Administration (FHA) loans,

VA loans or USDA loans offer unique financing options for people with lower credit

scores, low down payments or people looking to live in rural areas.

Depending on your unique situation, a loan type that caters towards specific pain

points might be more fitting for you than a traditional loan type. Explore more loans

for unique scenarios.

Shopping Around for Lenders Can Save You Thousands

Even though buying a home is often the biggest investment a person makes in their

lifetime, many buyers usually don’t shop around for a lender. Over half (54%) only

ever consider a single lender to finance their home. But shopping around for a

lender can prove to be beneficial to the buyer. That’s why the Consumer Financial

Protection Bureau recommends talking to at least three lenders when shopping for a

home loan.

By evaluating multiple lenders, you can compare rates and terms to get the best

option for your situation. If you only ever choose the first quote you get, you may be

missing out on a better rate from a different lender. You can use Zillow to find local

lenders in your area to help you through the process or compare rates anonymously.

NMLS 684537

2021 Financial Services of America, LLC -

Jim Pendleton NMLS 684537 ALL RIGHTS RESERVED